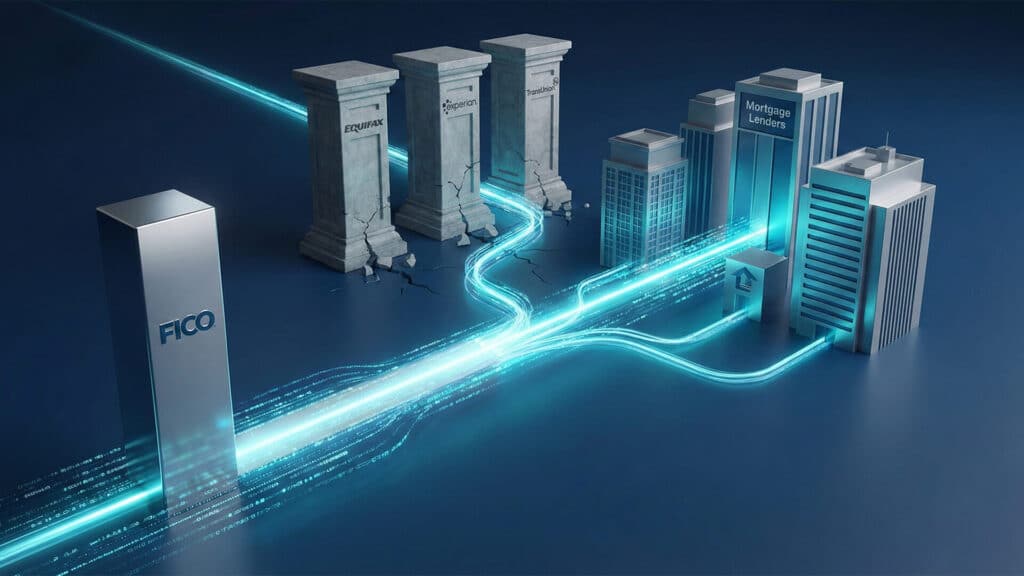

Fair Isaac Corp., the Montana-based company behind the FICO credit score, is shaking up the industry with a new pricing model aimed at mortgage lenders, per The Wall Street Journal. The shift could significantly weaken the grip of credit bureaus Experian, Equifax, and TransUnion, which have long controlled how credit scores are sold.

Under the new system, lenders will no longer need to purchase FICO scores through the credit bureaus. Instead, FICO will license scores directly to mortgage-tech resellers, who will then provide the scores to lenders, cutting out the bureau markups entirely.

“This new distribution model will allow lenders to avoid paying the current about 100 percent markup the credit bureaus currently charge for the FICO scores,” Raymon James analysts said, via Reuters.

FICO scores—which range from 300 to 850, with higher scores signaling lower credit risk—are used by nearly 90 percent of lenders, making them one of the most influential pieces of U.S. financial data. Cutting out bureau middlemen could lower operational costs for lenders, potentially reducing some mortgage-related fees for borrowers down the line.

Representatives from global investment bank Jeffries Group estimate that the change could hit bureau earnings by 10 to 15 percent, a major shake-up for an industry that has long profited from distributing FICO’s data.

FICO says the new setup introduces clearer, more competitive pricing. Under the revamped structure, lenders can choose between two pricing models rather than accepting one bureau-set rate.

“This change eliminates unnecessary mark-ups on the FICO Score and puts pricing model choice in the hands of those who use FICO Scores to drive mortgage decisions,” FICO CEO Will Lansing told CNBC.

The shift won’t impact personal credit scores directly, but it will reshape the industry around them. Over time, this could mean:

- Cleaner, simpler pricing behind mortgage applications

- Less control by the Big Three credit bureaus

- More competition among lenders and resellers

- Pressure on bureaus to improve accuracy and justify fees

In short: FICO just disrupted a decades-old system, and the ripple effects could change how lenders price future mortgages.